Trees

A reporting hierarchy structure consists of a number of trees.

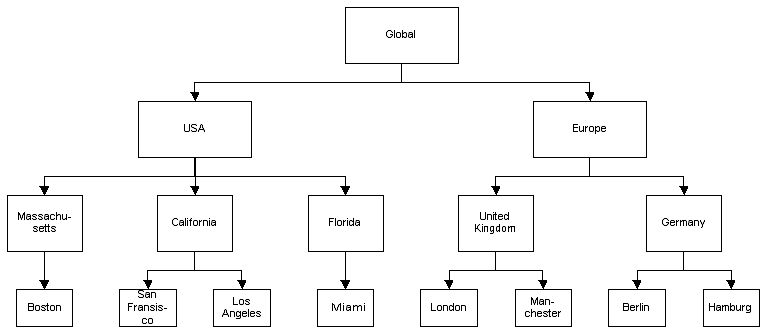

A tree is the topmost level in a hierarchy. For instance, a reporting hierarchy reflecting a geographically organized enterprise with offices in Europe and the USA could contain a single tree which sums up the figures from each of the geographical divisions in the organization, thus showing the grand total.

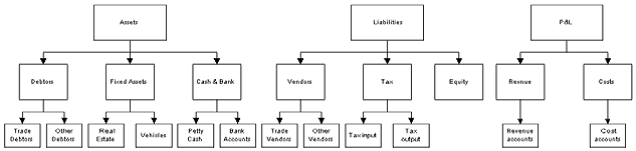

A reporting hierarchy can also contain multiple trees. Multiple trees should be used when the topmost level of information should show totals that are not related. A chart of accounts is an example of such a structure. Here, all the profit and loss accounts should be summed at the top level, and so should the balance sheet. However, the P&L, assets, and liabilities should not be added. Therefore, a reporting hierarchy used for a chart of accounts should consist of three trees, as shown in the simplified illustration below.

Please note that the structure in the illustration above is a very simplified example which does not necessarily reflect local accounting standards in your country. For instance, Equity may be required to be placed in a tree of its own.