Earned Value Cost Control

Although it is possible to set up a rudimentary cost management system that tracks budgeted and actual costs for a project, most organizations find such an approach far too limiting.

Budgeted and actual costs do not, in themselves, provide enough information for a manager to determine if the work currently in progress is, in fact, over- or under-budget. For example, assume you have planned an activity with an initial budget of $1000 spread evenly over the course of the activity. Midway through its planned duration, the activity has recorded actual costs of $500. Is the activity over or under budget? That depends entirely on an estimate of the physical completion of the activity. If the activity has achieved only 25% of its intended results, for example, it is clearly over budget (it has taken $500 to achieve what was originally planned to cost $250). If the activity is 50% complete, however, the same actual costs indicate that the activity is being performed according to its budget.

Since earned value is measured as a percentage of the budget, it is necessary to create a Performance Measurement Baseline (PMB) against which performance, or earned value, is measured. The PMB is a copy of the project plan at the beginning of the project and represents the approved budget. When approved budget changes occur, these changes are reflected in the PMB. Thus, you have a separation between the forecasted cost and the approved budgeted cost once the project is underway.

Measuring the work performed against a performance measurement baseline is typically called an earned value management system. To establish the systematic accounting of earned value, a project manager must have access to the following information:

- Performance Measurement Baseline

- Physical percent complete (an estimate of the work that has actually been performed by Time Now)

- Actual costs to date

- Forecast

With this information, the five principal elements of earned value cost control can be defined:

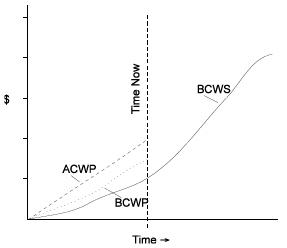

- Budgeted cost of work scheduled (BCWS): The budgeted cost of the work that should have been completed to Time Now, according to the PMB.

- Budget at complete (BAC): The total budgeted cost of the work according to the PMB.

- Budgeted cost of work performed (BCWP): The budgeted cost of the actual portion of the scheduled work that has been completed (or earned value)

- Actual cost of work performed (ACWP): The actual costs expended to perform the work completed

- Estimate at Complete (EAC): The estimated remaining costs plus the actual costs expended.

Typically, these values are represented as cumulative cost curves in graphic displays:

Taken together, these values (BCWS, BAC, BCWP, ACWP, and EAC) form the core of an earned value cost control system.

Related Topics

- Managing Costs Overview

- Cost and Schedule Variances

- Cost Control Features in Open Plan

- Understanding Open Plan Cost Calculations

- Using the Cost Calculations Dialog Box

- Cost Forecasting

- Using the Progress Calculations Dialog Box

- Histogram Preferences Earned Value Tab

- Displaying Earned Value Information on a Resource Histogram